Managing your books may seem simple, but small errors can quickly turn into expensive problems. By avoiding common bookkeeping mistakes, you protect your cash flow, stay compliant with tax rules, and keep your business financially healthy. Even something as basic as misclassifying an expense or missing a filing deadline can cost far more than the time it takes to do things correctly.

You need accurate records to understand how your business is performing and to make smart decisions. When you mix personal and business spending, delay reconciliations, or overlook cash flow, you risk running into issues that could have been prevented. These slip-ups not only create stress but may also lead to penalties or lost opportunities.

With the right approach, you can avoid the most common pitfalls. This article will walk you through why mistakes are so costly, how to prevent inaccurate records, and practical ways to stay on top of expenses, tax deadlines, and cash flow. You’ll also see how technology and professional support can make bookkeeping simpler and more reliable.

Why Bookkeeping Mistakes Are Costly

Bookkeeping errors affect more than just day-to-day numbers. They disrupt the accuracy of your records, create problems with compliance, and may expose you to financial or legal risks that are difficult and expensive to fix later.

Impact on Financial Reporting

When your records are inaccurate, your financial reporting becomes unreliable. This makes it hard to see whether your business is truly profitable or identify areas where costs are rising.

Poor reporting can also affect how you make decisions. For example, if expenses are misclassified, you may believe you have more cash available than you actually do. This can lead you to overspend, delay payments, or invest in new equipment before your business is ready.

Investors, lenders, and partners rely on accurate reports. If your figures do not reflect reality, you may lose credibility and struggle to secure funding. According to common bookkeeping mistakes highlighted by Precise Bookkeeping, failing to review financial reports regularly is one of the most expensive errors small businesses make.

Maintaining clear records ensures your Profit & Loss, Balance Sheet, and Cash Flow Statement provide a true picture of performance. This helps you make informed decisions and reduces the risk of mismanagement.

Consequences for Tax Filings

Errors in bookkeeping directly affect your tax filings. If expenses are not recorded correctly, you may miss deductions that lower your tax bill. On the other hand, overstating deductions or income can result in penalties.

Late or incorrect filings add unnecessary costs. HMRC imposes fines and interest for missed deadlines, and these can quickly add up. As noted in guides on bookkeeping mistakes, missing tax deadlines is one of the most common and costly issues for small businesses.

You also spend more time and money correcting mistakes later. Accountants may need to review months of records, which increases fees. By keeping accurate books throughout the year, you avoid last-minute stress and reduce the risk of errors when filing returns.

A simple step, such as keeping a separate savings account for tax payments, can help you stay prepared and avoid financial strain.

Risks of Audits and Penalties

Inaccurate records increase your chances of facing an audit. HMRC may flag inconsistencies in your filings, such as mismatched income or unusual expense claims. An audit requires you to provide detailed documentation, which is difficult if your books are incomplete or disorganised.

Penalties can be severe. If records show negligence or repeated mistakes, fines may be higher. In some cases, you could face ongoing monitoring, which adds more administrative burden.

Bookkeeping mistakes like mixing personal and business expenses often raise red flags. As explained in common errors identified by Pilot, these practices make it harder to prove your financial activity is legitimate.

Keeping accurate, well-organised records reduces the likelihood of an audit and protects you if one occurs. Reliable bookkeeping not only saves time but also demonstrates compliance, which helps maintain trust with tax authorities.

Inaccurate Financial Records and How to Prevent Them

Inaccurate financial records often lead to poor decisions, missed tax deductions, and compliance risks. Errors usually come from manual entry, disorganisation, or lack of review, but with the right systems and habits you can keep your bookkeeping reliable and up to date.

Common Causes of Inaccurate Records

Financial records become inaccurate when transactions are entered incorrectly, left incomplete, or categorised in the wrong accounts. Simple typing mistakes, transposed numbers, and forgotten receipts are frequent problems.

Mixing personal and business spending is another issue. Without clear separation, you risk overstating or understating expenses. This can distort profit figures and make tax reporting more difficult.

Poor organisation also plays a role. If you don’t have a consistent filing system for invoices, receipts, and statements, you may lose important documents. According to The Top 10 Bookkeeping Mistakes, disorganisation can also delay tax preparation and increase the risk of non-compliance.

Finally, failing to reconcile bank accounts regularly allows unnoticed errors and even fraud to slip into your records. Regular reconciliation ensures your books match actual account balances.

Preventing Data Entry Errors

You can reduce data entry mistakes by using accounting software that includes validation checks and automation. Many tools import transactions directly from your bank, reducing the need for manual entry.

Training is also important. Anyone entering financial data should understand the correct categories and procedures. Even small errors can affect reports and tax filings.

A useful practice is to double-check entries before finalising them. For high-value transactions, a second review by another person can add an extra layer of accuracy.

Automation tools, such as receipt scanning apps, also help. They capture data directly from invoices and receipts, reducing the chance of miskeyed numbers. As highlighted in Ensuring Accuracy in Bookkeeping, automation lowers human error and improves consistency.

Regular Review and Correction

Even with good systems, mistakes can still happen. Regular reviews of your financial records help you find and fix errors before they grow into bigger problems.

Schedule monthly or quarterly reviews where you compare reports, check balances, and confirm that expenses are categorised correctly. Keeping a checklist makes the process more efficient.

Bank reconciliation should be part of this routine. Matching your books with bank and credit card statements ensures that all income and expenses are recorded. The guide on common bookkeeping mistakes to avoid stresses that reconciliation is essential for accurate cash flow monitoring.

You should also keep supporting documents, such as receipts and invoices, to back up entries. This provides an audit trail and makes it easier to resolve discrepancies.

If you struggle to keep up with reviews, consider hiring a bookkeeper or accountant. A professional can provide regular oversight and ensure your records remain accurate and compliant.

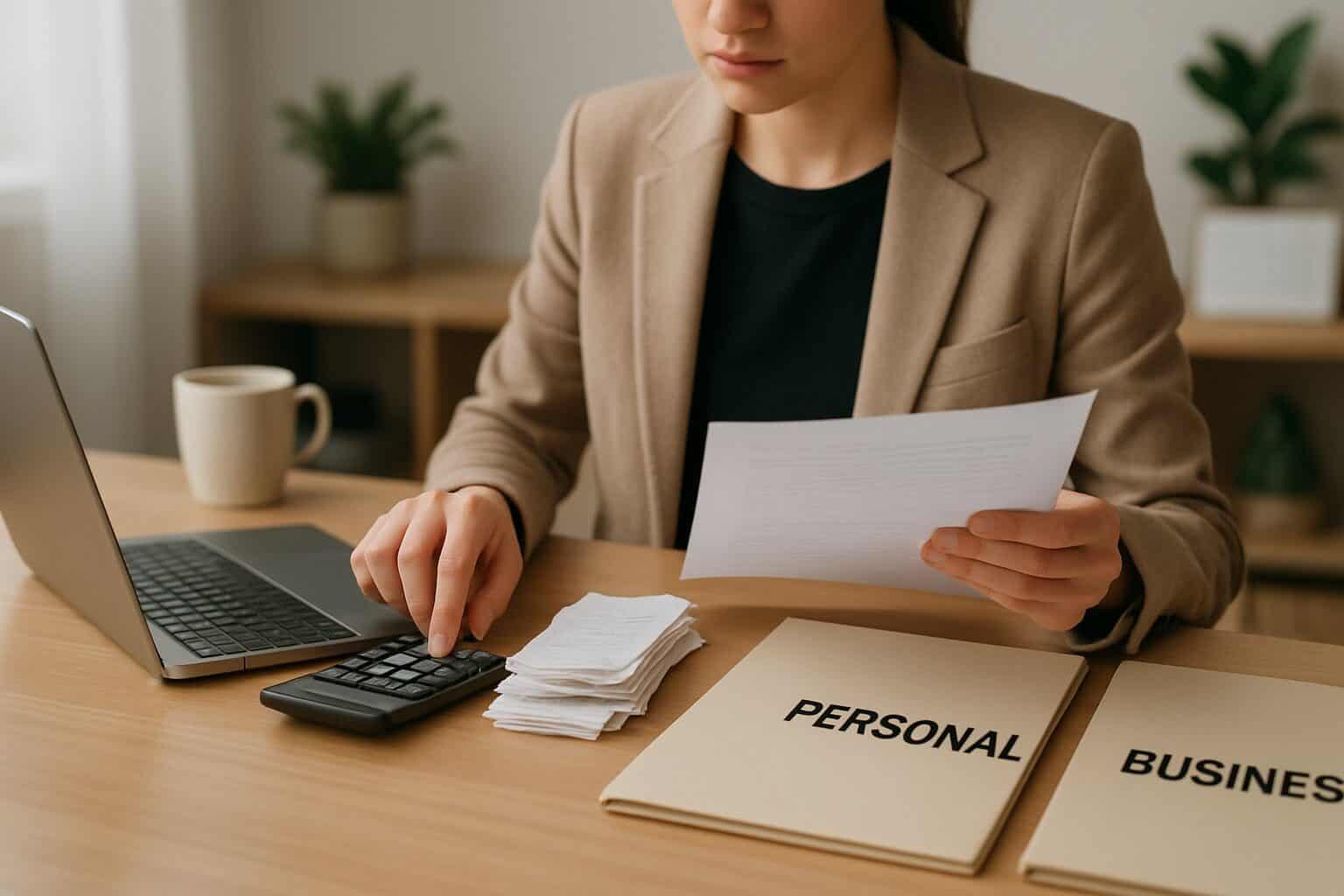

Mixing Personal and Business Finances

When you mix personal and business finances, you create confusion in your records and increase the risk of tax or legal issues. Keeping accounts separate helps you maintain accuracy, stay compliant, and make better financial decisions.

Dangers of Combining Accounts

Mixing personal and business finances makes it hard to see the true financial health of your company. If you use one account for everything, you blur the line between personal spending and business expenses. This can distort profit and loss statements and lead to inaccurate tax filings.

Tax authorities often view commingled accounts as a red flag. The IRS closely examines small businesses because misclassified expenses can reduce taxable income. If you cannot prove which costs are business-related, deductions may be disallowed, leaving you with higher tax bills.

Investors and lenders also rely on clean records. If your accounts are mixed, financial ratios such as debt-to-equity or cash flow projections may appear misleading. This can reduce your credibility and make it harder to secure loans or outside investment.

Even day-to-day management suffers. Without separation, you may struggle to track cash flow, set budgets, or forecast future expenses. This lack of clarity can limit growth and create operational risks.

How to Separate Finances Effectively

The simplest step is to open a dedicated business bank account. Use it only for income and expenses tied to your business. Pair it with a business credit card to keep transactions distinct and easier to categorise.

Adopting bookkeeping software helps you automate expense tracking and reduce errors. Many tools connect directly to your bank, making it easy to match receipts with transactions and generate reports. Regular reconciliation ensures your records stay accurate.

Set clear rules for spending. Always keep receipts, avoid using personal funds for business costs, and document every transfer between accounts. If you must move money, record it as an owner’s draw or capital contribution instead of leaving it unclear.

For added discipline, create written policies if you employ staff. Define which expenses are allowed, set approval limits, and require proof of purchase. These small steps protect your records and strengthen financial accountability.

Neglecting Regular Reconciliation

When you skip reconciling your accounts, you risk inaccurate reports, tax issues, and even unnoticed fraud. Regular reconciliation ensures your records match your bank and credit card statements, helping you maintain reliable financial data and better control over cash flow.

Why Regular Reconciliation Matters

Reconciling accounts means comparing your internal records with bank or credit card statements. This process confirms that every transaction is recorded correctly and no payments are missing or duplicated.

Without it, you may face errors in your financial statements. Inaccurate records can mislead you when making decisions and create problems during tax filing. Businesses that neglect this step often struggle with surprise expenses, overdraft fees, or missed deductions.

Regular reconciliation also helps detect fraud and unauthorised charges early. For example, if a payment leaves your bank but never appears in your books, you can investigate before the issue grows. According to Entikis Bookkeeping, failing to reconcile can also damage trust with lenders and investors who expect accurate reporting.

By keeping up with reconciliation, you maintain transparency, avoid costly mistakes, and ensure your financial health remains stable.

Steps for Effective Account Reconciliation

You can simplify reconciliation by using accounting software such as QuickBooks, which automates much of the matching process. These tools flag discrepancies, making it easier to spot missing or duplicate entries.

A good practice is to reconcile accounts monthly. Start by gathering your bank statements, credit card records, and accounting reports. Then, compare each transaction line by line, marking off items that match.

If you find discrepancies, investigate immediately. Common issues include bank fees, timing differences, or data entry errors. Create a checklist to make sure you review all accounts, not just your main bank account.

For small businesses, setting aside a fixed time each month reduces the chance of overlooking this task. Consistency ensures your books stay accurate, giving you confidence in your financial data and smoother tax preparation.

Poor Expense Tracking and Misclassification

When you fail to record expenses properly or assign them to the wrong category, your financial reports lose accuracy. This can affect cash flow management, tax deductions, and decision-making. Even small bookkeeping mistakes in expense tracking can create larger compliance or reporting issues later.

Tracking All Business Expenses

You need to track every business expense, no matter how small. Missing receipts or unrecorded payments can distort your accounts and reduce the deductions you can claim. For example, travel costs, software subscriptions, and office supplies should all be logged consistently.

Many businesses still rely on manual methods, which often leads to errors and wasted time. Manual expense tracking can cause productivity loss when employees spend hours collecting receipts and filling forms instead of focusing on work. Using digital tools or accounting software reduces this risk by automating data entry and storing receipts securely.

A simple structure helps you stay organised:

| Expense Type | Example Items | Record Method |

|---|---|---|

| Travel | Train tickets, fuel, hotels | Digital receipts, mileage logs |

| Office Supplies | Stationery, printers, ink | Scanned receipts, software logs |

| Subscriptions | Accounting software, email tools | Automatic monthly entries |

By recording transactions promptly and keeping receipts in a central system, you create a reliable audit trail. This makes tax filing easier and strengthens your financial management.

Correctly Categorising Transactions

Misclassifying expenses is one of the most common bookkeeping mistakes. When you place costs in the wrong category, your financial statements become misleading. This can also affect tax reporting, as deductions may be missed or wrongly applied.

You should maintain a clear chart of accounts with categories such as assets, liabilities, equity, income, and expenses. Regularly review these categories to ensure they match your business activities. For example, marketing costs should not be placed under general office expenses, and contractor payments must not be treated as employee wages.

Incorrect categorisation can also cause problems during audits or when applying for loans. Financial institutions expect accurate reporting, and errors can reduce your credibility. Training staff on proper categorisation methods or using software with automated classification features can help reduce mistakes.

By keeping categories consistent and accurate, you ensure that your reports reflect the true financial position of your business. This allows you to make decisions based on reliable data while staying compliant with tax rules.

Overlooking Cash Flow Management

Many businesses fail not because they lack profit but because they mismanage the movement of money in and out of the company. Poor tracking of cash flow can lead to missed payments, strained supplier relationships, and difficulty meeting payroll.

Understanding Cash Flow

Cash flow refers to the timing of money entering and leaving your business. Even if your balance sheet shows a profit, you can still face problems if your accounts receivable take too long to collect. A cash flow statement helps you track this movement and identify gaps before they become serious.

When you overlook cash flow, you may underestimate upcoming expenses. For example, you might have invoices due for accounts payable while waiting for customer payments. Without planning, this mismatch can leave you short of funds.

It is also important to distinguish between profit and cash flow. Profit reflects earnings on paper, but cash flow reveals your actual ability to pay bills. According to Cash Flow Frog, many businesses run into trouble by confusing these two measures.

By reviewing your cash flow statement regularly, you gain a clear picture of your financial position. This allows you to adjust spending, delay non-essential purchases, or negotiate better payment terms with suppliers.

Maintaining a Healthy Cash Flow

To keep your cash flow stable, you need consistent monitoring. Set up a schedule to review your cash flow statement alongside your balance sheet and income statement. This ensures you see how daily operations affect your liquidity.

Practical steps can make a difference:

- Invoice quickly and follow up on late payments.

- Negotiate accounts payable terms to align with your receivables.

- Build a cash reserve to cover unexpected expenses.

- Forecast cash flow at least three to six months ahead.

As noted by Love Accountancy, even profitable companies can collapse if they ignore cash flow forecasting. Planning helps you avoid sudden shortages.

Maintaining healthy cash flow also means controlling costs. Review recurring expenses and cut unnecessary spending. Small improvements in expense management can free up funds and reduce pressure on your accounts payable cycle.

By combining forecasting, cost control, and timely collections, you create a system that supports both short-term stability and long-term growth.

Missing Tax Deadlines and Failing to Prepare for Tax Season

Late tax filings often lead to penalties, interest charges, and unnecessary stress. Careful preparation and a system to track important dates can help you stay compliant and avoid last‑minute problems.

Common Tax Season Pitfalls

One of the most frequent mistakes is missing the official filing date. In the UK, the online Self Assessment deadline falls on 31 January, while paper returns are due by 31 October. Missing either date results in automatic fines, even if you owe no tax.

Another issue is failing to keep accurate records throughout the year. Without organised receipts, invoices, or bank statements, you may scramble to complete your return. This increases the risk of errors that could trigger HMRC enquiries.

Some taxpayers also underestimate how long it takes to gather information. Employment income, rental earnings, dividends, and pensions must all be reported. Forgetting even a small source of income can lead to penalties.

Businesses often face additional complexity, such as VAT returns and corporation tax deadlines. Overlooking these obligations can affect cash flow and create avoidable financial strain.

You can read more about common tax mistakes that taxpayers make, including missed deadlines and incomplete filings.

Setting Up Reliable Reminders

To avoid late submissions, create a reliable reminder system. Start by marking all key deadlines in your calendar, including Self Assessment, VAT, and corporation tax dates. Use both digital and physical reminders for extra security.

Many people benefit from setting alerts well before the due date. For example, schedule a reminder 30 days in advance, then another one week before. This gives you enough time to resolve missing paperwork or technical issues.

Consider using HMRC’s online services, which allow you to view deadlines and submit returns electronically. Digital tools and accounting software can also send automated reminders and track filing progress.

If you work with an accountant, agree on a timeline for sharing documents. Providing information early ensures they have time to review and file accurately. This reduces the risk of late penalties and helps you manage payments in advance.

For more tips on avoiding late submissions, see how missing tax deadlines can impact your obligations and what steps you can take to stay on track.

The Role of Technology and Professional Help

Using the right tools and support can prevent costly errors in your financial records. Modern bookkeeping relies on reliable software and, in many cases, outside professionals who can manage tasks more efficiently and accurately than handling everything on your own.

Choosing the Right Accounting Software

Selecting the right accounting software is one of the most important steps in keeping your books accurate. Tools like QuickBooks, Xero, or FreshBooks can automate invoicing, track expenses, and generate reports with minimal manual input. This reduces the risk of human error and helps you stay compliant with tax requirements.

When comparing bookkeeping software, pay attention to features such as:

- Bank integration for automatic transaction imports

- Customisable reports for better financial insights

- Cloud access so you can view data from anywhere

- Scalability to grow with your business

Costs vary, but many providers offer monthly plans that can be tailored to your needs. Choosing software that integrates with other tools you already use, such as payroll or inventory systems, will save time and reduce duplicate data entry.

Modern bookkeeping tools have become central to business management, turning what was once a paper-heavy process into a streamlined digital system. For example, technology in bookkeeping now uses automation and cloud-based solutions to improve accuracy and efficiency.

Benefits of Outsourcing Bookkeeping

Outsourcing bookkeeping can free up your time and reduce the risk of errors caused by inexperience. Professional bookkeepers and accountants bring expertise in tax law, compliance, and reporting that most business owners do not have.

You gain access to up-to-date knowledge of regulations, which helps you avoid penalties. Outsourcing also provides a second set of eyes on your records, making it easier to identify mistakes or irregularities early.

Some firms offer flexible packages, letting you choose between full-service bookkeeping or support with specific tasks, such as payroll or VAT returns. This makes outsourcing cost-effective for small and medium-sized businesses.

As technology reshapes bookkeeping services, outsourcing providers now combine human expertise with automation. This gives you accurate reporting, faster turnaround times, and secure document handling without the need to manage everything in-house.

Frequently Asked Questions

Bookkeeping mistakes often happen when entries are recorded incorrectly, financial data is not reviewed, or accounting methods are misunderstood. You can reduce errors by staying organised, following clear processes, and seeking professional guidance when needed.

What are some typical errors to avoid when recording entries in journals or ledgers?

You should avoid entering transactions twice, omitting expenses, or misclassifying income. Mixing business and personal spending is another common mistake that creates confusion in your records. Errors like these can distort your financial statements and lead to compliance issues.

How can one rectify mistakes once they have been identified in bookkeeping records?

Correct errors by making adjusting entries rather than deleting or overwriting the original record. Keep a clear audit trail showing what was changed and why. If you are unsure, consult a qualified accountant to ensure your correction is accurate and compliant.

In what ways can bookkeepers ensure accuracy when unsure about the categorisation of a new transaction?

If you are uncertain, seek guidance from a chart of accounts tailored to your business. You can also ask your accountant or bookkeeper for clarification. Avoid guessing, as this can lead to long-term inaccuracies, as noted in common bookkeeping mistakes.

What are the disadvantages of using the cash accounting method in bookkeeping?

Cash accounting may give you a misleading picture of profitability because it only records money when it changes hands. This method does not show outstanding invoices or unpaid bills, which can make it harder to manage cash flow and plan for future expenses.

What essential steps should be taken to maintain proper bookkeeping?

Keep your records up to date, reconcile bank statements regularly, and store receipts for at least seven years. Use accounting software to automate repetitive tasks and reduce errors. Regularly review financial reports to identify issues early.

What should you understand about bookkeeping to manage financial records effectively?

You need to understand how to categorise transactions, read financial statements, and follow tax obligations. Knowing the difference between assets, liabilities, income, and expenses is essential. With this knowledge, you can make informed financial decisions and avoid costly bookkeeping errors.